March 16, 2014

Liquidation Trusts

Coauthored by Evan T. Miller and Marla H. Norton

Liquidating trusts are organized for the primary purpose of liquidating assets transferred to them for distribution to trust beneficiaries. Liquidating trusts can be effective tools to wind down any business enterprise, including debtors in Chapter 11 bankruptcy cases and entities that dissolve outside of bankruptcy. Whether the trust is the product of a bankruptcy plan or a state law plan of dissolution, certain factors must be considered. To find out more, Lawyer Monthly hears from Ashley B. Stitzer, Evan T. Miller and Marla H. Norton, Attorneys at Bayard, P.A.

The US Bankruptcy Code seeks to promote the effective administration and settlement of a debtor's assets and liabilities within a limited frame of time. To that end, in a Chapter 11 case, a debtor's exclusive right to file a plan is limited to 120 days (subject to extensions for cause), but once a plan is confirmed, the bankruptcy estate ceases to exist and the debtor loses its status as debtor in possession, including its authority to act as a bankruptcy trustee and pursue estate claims. Section 1123(b)(3)(B) of the Bankruptcy Code allows this prospect to be avoided. It states that a plan may provide for the retention and enforcement by the debtor, by the trustee, or by a representative of the estate appointed for such purpose, of any such claim or interest. Absent this provision, a debtor would be required to investigate and prosecute all avoidance and other causes of action prior to confirming a plan, which may take years.

Section 1123(b) (3) of the Bankruptcy Code facilitates the use of a liquidating trust for prompt administration of the estate by providing post-confirmation standing to an appointed representative of the estate to enforce claims and interests. By establishing a liquidating trust pursuant to section 1123(b)(3) in a confirmed plan of reorganization or liquidation, a debtor can transfer causes of action and other assets to a trust, for future liquidation and distribution to the debtor's creditors, and avoid delaying plan confirmation. The creditors become the trust beneficiaries and their claims are paid from trust assets by a waterfall established pursuant to the plan.

In conjunction with the other provisions of the Bankruptcy Code that require a disclosure statement and plan to provide "adequate information" for a claim or interest holder to make an informed judgment about the plan, Section 1123(b)(3) effectively provides notice to creditors of retention and prospective enforcement of claims that may enlarge the estate's assets for distribution. A plan must expressly retain claims to preserve a liquidating trust's standing to pursue them after plan confirmation. If the plan fails to sufficiently preserve the claim, the claim may be subject to an attack on the basis of subject matter jurisdiction. The degree of specificity required in identifying preserved claims varies from jurisdiction to jurisdiction. When drafting a plan and liquidating trust agreement, parties should ensure that the applicable jurisdictional prerequisites are met.

If a liquidating trustee's standing to enforce estate claims, as an appointed representative under Section 1123(b)(3)(B), is challenged, the trustee must first demonstrate that he or she has been appointed to enforce the claim. The appointment is generally done in the plan, confirmation order and trust agreement. The liquidating trustee must also demonstrate that he or she qualifies as a representative of the estate. A trustee qualifies as a representative of the estate if a successful recover would benefit, directly or indirectly, the debtor's the creditors that are beneficiaries of the trust.

Treasury Regulation 301.7701-4(d), 26 CFR § 301.7701-4(d) ("Treas. Reg. 301.7701-4(d)") provides for establishment of a liquidating trust as a grantor trust, such that it will be a pass-through entity for tax purposes, without an entity-level tax. In 1994, the Internal Revenue Service (the "IRS") issued Revenue Procedure 94-45 ("Rev. Proc. 94-45"), which established guidelines applicable to liquidating trusts formed to implement a Chapter 11 plan, which are similar to the considerations applicable to a liquidating trust outside bankruptcy. If followed, these guidelines should ensure that the establishment of the trust will be treated as a transfer from the bankruptcy estate to the beneficiaries followed by a deemed transfer by the beneficiaries to the liquidating trust. Rev. Proc. 94-45 lists twelve conditions which, if met, will generally result in the issuance by the IRS of an advance determination classifying the trust as a liquidating trust under Treas. Reg. 301.7701-4(d). While Rev. Proc. 94-45 notes that it does not define as a matter of law the circumstances under which an organization will be classified as a liquidating trust for income tax purposes, the conditions are commonly incorporated into plans and liquidating trust agreements whether or not an advance ruling is sought.

Under Rev. Proc. 94-45, the plan and disclosure statement must explain how the bankruptcy estate will treat the transfer of its assets to the trust for federal income tax purposes. A transfer to a liquidating trust for the benefit of creditors must be treated for all purposes of the Revenue Code as a transfer to creditors to the extent that the creditors are beneficiaries of the trust. The transfer will be treated as a deemed transfer to the beneficiary-creditors followed by a deemed transfer by the beneficiary-creditors to the trust. The plan, disclosure statement, and trust agreement must provide that the beneficiaries of the trust will be treated as the grantors and deemed owners of the trust and that the trust instrument (or plan if a separate trust agreement does not exist) requires the trustee to file returns for the trust as a grantor trust pursuant to section 1.671-4(a) of the Income Tax Regulations, 26 CFR § 1.671-4(a). The plan, disclosure statement, and any separate trust instrument must provide for consistent valuations of the transferred property by the trustee and the creditors, and those valuations must be used for all federal income tax purposes. Finally, a liquidating trust may lose its grantor trust status "if the liquidation is unreasonably prolonged or if the liquidation purpose becomes so obscured by business activities that the declared purpose of liquidation can be said to be lost or abandoned." 26 CFR § 301.7701-4(d).

Additional considerations include retaining bankruptcy court jurisdiction in the plan and trust agreement so that a liquidating trustee can seek court approval of certain actions and decisions made on behalf of the trust. An oversight committee is often utilized as well to oversee the liquidating trustee's certain decisions and actions. Additionally, exculpation and release provisions provide further liability protection to the liquidating trustee.

Liquidating trusts created under bankruptcy plans often vest their trustees with authority to prosecute avoidance and related actions against the creditors and third parties. Trustees may initiate these actions against parties with little to no connection to the United States raising unsettled questions over jurisdiction. See, e.g., Weitz v. Ascot (In re Waste2Energy Holdings, Inc.), Case No. 12-50819-KJC (Bankr. D. Del.). As the volume of crossborder Chapter 11 cases continues to increase, liquidating trustees prosecuting estate causes of action may face more personal jurisdiction challenges.

Bayard's Bankruptcy Group has long provided services to debtors, official committees of unsecured creditors and equity holders, trustees, purchasers and lenders in bankruptcy cases. It also represents parties in other insolvency proceedings, including receiverships, assignments for the benefit of creditors, dissolution proceedings under state law and rehabilitations and liquidations of insurance companies. The Bankruptcy Group works regularly with clients through all phases of the reorganization or liquidation of troubled businesses, including out-of-court workouts and distressed asset acquisitions. For questions concerning insolvency law, including US bankruptcy law and insurance company insolvency law, please contact Ashley Stitzer at (302) 429-4242 or AStitzer@bayardlaw.com.

A liquidating trust can also be a useful tool outside of bankruptcy. Business organizations that are dissolving may wish to use a liquidating trust in order to delegate the administration of the winding up process. While the managers of a business may be well-suited for the tasks of running a going concern, their talents may not be optimal for the winding down process, which consists of marshaling and selling assets, making distributions to and communicating with creditors and estimating reserves. These tasks may not justify the salaries being paid to the management team, which may wish to move on to new challenges. These considerations may tip the scales in favor of setting up a liquidation vehicle and bringing in an administrator experienced with winding down operations.

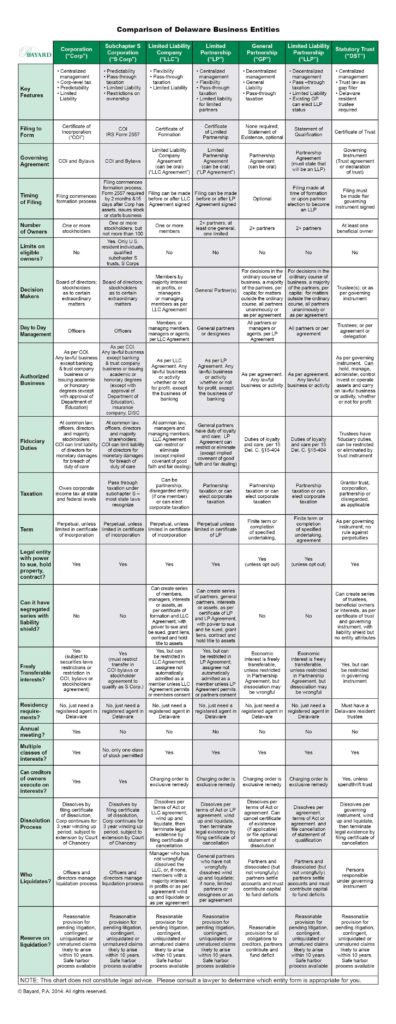

The dissolution procedures for a business organization vary, depending on the type of entity and the jurisdiction in which it is formed. For example, as shown on the below chart, a Delaware corporation continues to exist for a period of three years following the filing of a certificate

of dissolution, but a Delaware partnership or limited liability company's legal existence continues indefinitely following an event of dissolution, until a certificate of cancellation is filed. For an entity with a complicated asset portfolio, it may make sense to transfer all assets, rights, and causes in action to a liquidating trust that can liquidate assets and investments over time, avoiding market dips and other timing concerns. Moreover, to the extent that entities like partnerships and limited liability companies are not permitted to engage in business once they are dissolved, the liquidating trust may be authorized to operate or hold certain assets to take advantage of economic factors (but subject to tax considerations).

Other timing considerations may be presented by contingent, unliquidated or unmatured claims. As reflected on the below chart, Delaware corporations, partnerships and limited liability companies must make reasonable reserve for all pending litigation, and for claims and obligations that have not yet accrued but, based upon facts known to management, are likely to accrue within ten years following the dissolution. While Delaware corporations may take advantage of a "safe harbor" process that involves notice to creditors and guidance of the Delaware Court of Chancery in approving reserves, this process is rarely invoked and is not available for other Delaware entity forms. Failure to make "reasonable reserve" is a basis for liability on the part of the person(s) conducting the liquidation. The terms of a liquidating trust may permit the trustee(s) to invest the proceeds of liquidation of assets (typically in short-term assets) and await the outcome of litigation or the occurrence or lapse of conditions affecting the magnitude or likelihood of claims, subject to the requirement of Treas. Reg. 301.7701-4(d) that "if the liquidation is unreasonably prolonged orif the liquidation purpose becomes so obscured by business activities," the trust may lose its status as a liquidating trust for tax purposes. Moreover, by entrusting the liquidation process to a liquidating trust charged with establishing appropriate reserves, management can take comfort that they have discharged their duties. Arguably, by using a Delaware statutory trust or an equivalent vehicle for a liquidating trust, the exculpation and indemnification provisions applicable to the trustees can be used to protect them from liability.

Many of the liquidating trusts formed both within and outside the bankruptcy environment are organized as Delaware statutory trusts ("DSTs") pursuant to the Delaware Statutory Trust Act, 12 Del. C. § 3801 et seq. (the "DST Act"). The DST Act does not require that a DST be organized for profit, and contains a variety of features that are advantageous in dealing with the many competing considerations in a liquidating trust. To the extent that the persons winding up the debtor or other liquidating entity may have claims to pursue or defend, a DST is a separate legal entity. The DST Act permits a trustee to take direction from other parties, whether beneficiaries, advisors, a grantor or other interested or independent parties. Thus a management or oversight committee may be appointed to make certain determinations, to monitor the trustee's activities. The DST Act also empowers a trustee to delegate some or nearly all of its powers without rendering the delegee liable as a trustee. Of critical importance are the provisions of the DST Act permitting drafters of a trust governing instrument to restrict, modify or eliminate fiduciary duties of trustees and other persons managing a DST, subject to the implied contractual

covenant of good faith and fair dealing.

The annual maintenance costs for a DST are fairly nominal - the trust pays no annual maintenance fee to the Delaware Secretary of State. In addition to the fees payable to the liquidating agent, or liquidating trustee, if the liquidating trustee is not an individual Delaware resident, or a Delaware banking institution or trust company or federally chartered bank or trust company with its principal place of business in Delaware, the trust will need to engage a trustee meeting that description. Fortunately, there are individuals and institutions in Delaware that make a business of providing Delaware statutory trustee services for a fairly nominal fee (a few thousand dollars a year) who will undertake the limited role of qualifying the trust as a DST. Of course, many local banking institutions will also provide the more substantive services, for a higher fee.

Additional factors to consider include tax and securities implications. As noted above, most liquidation trusts are structured as grantor trusts for tax purposes, and the IRS has established standards pursuant to Treas. Reg. 301.7701-4(d) applicable to liquidating trusts that, if followed, should ensure that they are not subject to entity-level income taxes. If the trust term will be longer than a few years, it may be prudent to seek an IRS determination letter that the trust will qualify for grantor trust tax treatment. In addition, where a public company with over $10,000,000 in assets at least one registered class of securities held by at least 500 stockholders, consideration must be given to whether the interests in the liquidating trust will be "equity securities" such that the trust must register the interest with the Securities and

Exchange Commission. For these and other reasons, it is important to secure experienced professionals to assist with the formation of a liquidation trust.

Bayard's entity law group has experience working with the full array of Delaware business organizations, including statutory trusts, corporations, general partnerships, limited partnerships, limited liability partnerships and limited liability companies. Each of these entity types presents different considerations as to establishment, operation, management, liability, scope of authority and dissolution. While Delaware corporations are highly regarded due to Delaware's progressive and regularly updated corporate statutes, the substantial body of interpretive case law, which promotes predictability, specialized and well-respected Delaware Court of Chancery and responsive and technologically advanced Division of Corporations, Delaware alternative entities are known for their flexibility and share in a growing body of case law, and the benefits of access to the Court of Chancery and Division of Corporations. Bayard also has experienced litigators capable of handling a variety of entity law litigation matters, including seeking the appointment of receivers for dissolved companies and seeking approval of a corporate plan of liquidation under the so called "safe harbor" liquidation procedures. For questions regarding Delaware entity law, please contact Marla Norton at (302) 429-4214 or MNorton@bayardlaw.com.

For your convenience we are providing an excerpt of a chart we have prepared which provides an overview the different features of each entity type, highlighting the default rules relating to liquidation and winding up of each. The full table can be viewed on Bayard's web site at www.bayardlaw.com.

First published in Lawyer Monthly, March 2014. Link to article.

Liquidating trusts are organized for the primary purpose of liquidating assets transferred to them for distribution to trust beneficiaries. Liquidating trusts can be effective tools to wind down any business enterprise, including debtors in Chapter 11 bankruptcy cases and entities that dissolve outside of bankruptcy. Whether the trust is the product of a bankruptcy plan or a state law plan of dissolution, certain factors must be considered. To find out more, Lawyer Monthly hears from Ashley B. Stitzer, Evan T. Miller and Marla H. Norton, Attorneys at Bayard, P.A.

The US Bankruptcy Code seeks to promote the effective administration and settlement of a debtor's assets and liabilities within a limited frame of time. To that end, in a Chapter 11 case, a debtor's exclusive right to file a plan is limited to 120 days (subject to extensions for cause), but once a plan is confirmed, the bankruptcy estate ceases to exist and the debtor loses its status as debtor in possession, including its authority to act as a bankruptcy trustee and pursue estate claims. Section 1123(b)(3)(B) of the Bankruptcy Code allows this prospect to be avoided. It states that a plan may provide for the retention and enforcement by the debtor, by the trustee, or by a representative of the estate appointed for such purpose, of any such claim or interest. Absent this provision, a debtor would be required to investigate and prosecute all avoidance and other causes of action prior to confirming a plan, which may take years.

Section 1123(b) (3) of the Bankruptcy Code facilitates the use of a liquidating trust for prompt administration of the estate by providing post-confirmation standing to an appointed representative of the estate to enforce claims and interests. By establishing a liquidating trust pursuant to section 1123(b)(3) in a confirmed plan of reorganization or liquidation, a debtor can transfer causes of action and other assets to a trust, for future liquidation and distribution to the debtor's creditors, and avoid delaying plan confirmation. The creditors become the trust beneficiaries and their claims are paid from trust assets by a waterfall established pursuant to the plan.

In conjunction with the other provisions of the Bankruptcy Code that require a disclosure statement and plan to provide "adequate information" for a claim or interest holder to make an informed judgment about the plan, Section 1123(b)(3) effectively provides notice to creditors of retention and prospective enforcement of claims that may enlarge the estate's assets for distribution. A plan must expressly retain claims to preserve a liquidating trust's standing to pursue them after plan confirmation. If the plan fails to sufficiently preserve the claim, the claim may be subject to an attack on the basis of subject matter jurisdiction. The degree of specificity required in identifying preserved claims varies from jurisdiction to jurisdiction. When drafting a plan and liquidating trust agreement, parties should ensure that the applicable jurisdictional prerequisites are met.

If a liquidating trustee's standing to enforce estate claims, as an appointed representative under Section 1123(b)(3)(B), is challenged, the trustee must first demonstrate that he or she has been appointed to enforce the claim. The appointment is generally done in the plan, confirmation order and trust agreement. The liquidating trustee must also demonstrate that he or she qualifies as a representative of the estate. A trustee qualifies as a representative of the estate if a successful recover would benefit, directly or indirectly, the debtor's the creditors that are beneficiaries of the trust.

Treasury Regulation 301.7701-4(d), 26 CFR § 301.7701-4(d) ("Treas. Reg. 301.7701-4(d)") provides for establishment of a liquidating trust as a grantor trust, such that it will be a pass-through entity for tax purposes, without an entity-level tax. In 1994, the Internal Revenue Service (the "IRS") issued Revenue Procedure 94-45 ("Rev. Proc. 94-45"), which established guidelines applicable to liquidating trusts formed to implement a Chapter 11 plan, which are similar to the considerations applicable to a liquidating trust outside bankruptcy. If followed, these guidelines should ensure that the establishment of the trust will be treated as a transfer from the bankruptcy estate to the beneficiaries followed by a deemed transfer by the beneficiaries to the liquidating trust. Rev. Proc. 94-45 lists twelve conditions which, if met, will generally result in the issuance by the IRS of an advance determination classifying the trust as a liquidating trust under Treas. Reg. 301.7701-4(d). While Rev. Proc. 94-45 notes that it does not define as a matter of law the circumstances under which an organization will be classified as a liquidating trust for income tax purposes, the conditions are commonly incorporated into plans and liquidating trust agreements whether or not an advance ruling is sought.

Under Rev. Proc. 94-45, the plan and disclosure statement must explain how the bankruptcy estate will treat the transfer of its assets to the trust for federal income tax purposes. A transfer to a liquidating trust for the benefit of creditors must be treated for all purposes of the Revenue Code as a transfer to creditors to the extent that the creditors are beneficiaries of the trust. The transfer will be treated as a deemed transfer to the beneficiary-creditors followed by a deemed transfer by the beneficiary-creditors to the trust. The plan, disclosure statement, and trust agreement must provide that the beneficiaries of the trust will be treated as the grantors and deemed owners of the trust and that the trust instrument (or plan if a separate trust agreement does not exist) requires the trustee to file returns for the trust as a grantor trust pursuant to section 1.671-4(a) of the Income Tax Regulations, 26 CFR § 1.671-4(a). The plan, disclosure statement, and any separate trust instrument must provide for consistent valuations of the transferred property by the trustee and the creditors, and those valuations must be used for all federal income tax purposes. Finally, a liquidating trust may lose its grantor trust status "if the liquidation is unreasonably prolonged or if the liquidation purpose becomes so obscured by business activities that the declared purpose of liquidation can be said to be lost or abandoned." 26 CFR § 301.7701-4(d).

Additional considerations include retaining bankruptcy court jurisdiction in the plan and trust agreement so that a liquidating trustee can seek court approval of certain actions and decisions made on behalf of the trust. An oversight committee is often utilized as well to oversee the liquidating trustee's certain decisions and actions. Additionally, exculpation and release provisions provide further liability protection to the liquidating trustee.

Liquidating trusts created under bankruptcy plans often vest their trustees with authority to prosecute avoidance and related actions against the creditors and third parties. Trustees may initiate these actions against parties with little to no connection to the United States raising unsettled questions over jurisdiction. See, e.g., Weitz v. Ascot (In re Waste2Energy Holdings, Inc.), Case No. 12-50819-KJC (Bankr. D. Del.). As the volume of crossborder Chapter 11 cases continues to increase, liquidating trustees prosecuting estate causes of action may face more personal jurisdiction challenges.

Bayard's Bankruptcy Group has long provided services to debtors, official committees of unsecured creditors and equity holders, trustees, purchasers and lenders in bankruptcy cases. It also represents parties in other insolvency proceedings, including receiverships, assignments for the benefit of creditors, dissolution proceedings under state law and rehabilitations and liquidations of insurance companies. The Bankruptcy Group works regularly with clients through all phases of the reorganization or liquidation of troubled businesses, including out-of-court workouts and distressed asset acquisitions. For questions concerning insolvency law, including US bankruptcy law and insurance company insolvency law, please contact Ashley Stitzer at (302) 429-4242 or AStitzer@bayardlaw.com.

A liquidating trust can also be a useful tool outside of bankruptcy. Business organizations that are dissolving may wish to use a liquidating trust in order to delegate the administration of the winding up process. While the managers of a business may be well-suited for the tasks of running a going concern, their talents may not be optimal for the winding down process, which consists of marshaling and selling assets, making distributions to and communicating with creditors and estimating reserves. These tasks may not justify the salaries being paid to the management team, which may wish to move on to new challenges. These considerations may tip the scales in favor of setting up a liquidation vehicle and bringing in an administrator experienced with winding down operations.

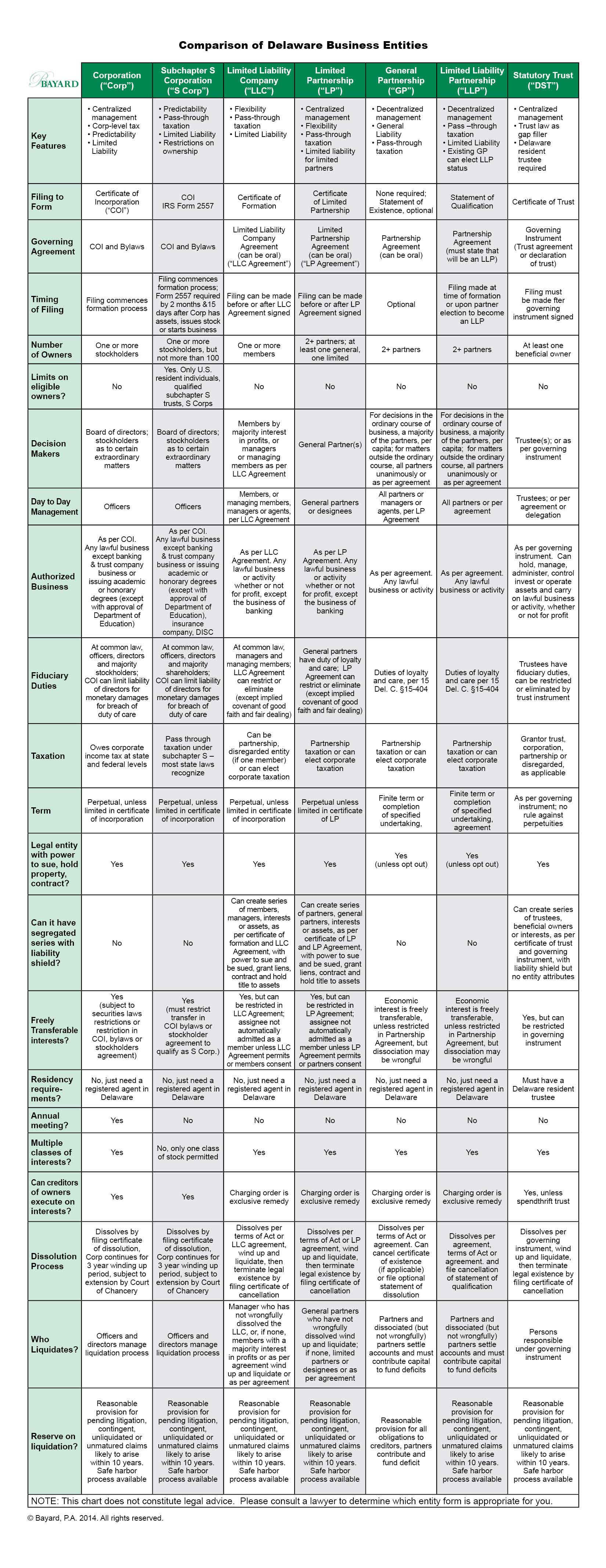

The dissolution procedures for a business organization vary, depending on the type of entity and the jurisdiction in which it is formed. For example, as shown on the below chart, a Delaware corporation continues to exist for a period of three years following the filing of a certificate

of dissolution, but a Delaware partnership or limited liability company's legal existence continues indefinitely following an event of dissolution, until a certificate of cancellation is filed. For an entity with a complicated asset portfolio, it may make sense to transfer all assets, rights, and causes in action to a liquidating trust that can liquidate assets and investments over time, avoiding market dips and other timing concerns. Moreover, to the extent that entities like partnerships and limited liability companies are not permitted to engage in business once they are dissolved, the liquidating trust may be authorized to operate or hold certain assets to take advantage of economic factors (but subject to tax considerations).

Other timing considerations may be presented by contingent, unliquidated or unmatured claims. As reflected on the below chart, Delaware corporations, partnerships and limited liability companies must make reasonable reserve for all pending litigation, and for claims and obligations that have not yet accrued but, based upon facts known to management, are likely to accrue within ten years following the dissolution. While Delaware corporations may take advantage of a "safe harbor" process that involves notice to creditors and guidance of the Delaware Court of Chancery in approving reserves, this process is rarely invoked and is not available for other Delaware entity forms. Failure to make "reasonable reserve" is a basis for liability on the part of the person(s) conducting the liquidation. The terms of a liquidating trust may permit the trustee(s) to invest the proceeds of liquidation of assets (typically in short-term assets) and await the outcome of litigation or the occurrence or lapse of conditions affecting the magnitude or likelihood of claims, subject to the requirement of Treas. Reg. 301.7701-4(d) that "if the liquidation is unreasonably prolonged orif the liquidation purpose becomes so obscured by business activities," the trust may lose its status as a liquidating trust for tax purposes. Moreover, by entrusting the liquidation process to a liquidating trust charged with establishing appropriate reserves, management can take comfort that they have discharged their duties. Arguably, by using a Delaware statutory trust or an equivalent vehicle for a liquidating trust, the exculpation and indemnification provisions applicable to the trustees can be used to protect them from liability.

Many of the liquidating trusts formed both within and outside the bankruptcy environment are organized as Delaware statutory trusts ("DSTs") pursuant to the Delaware Statutory Trust Act, 12 Del. C. § 3801 et seq. (the "DST Act"). The DST Act does not require that a DST be organized for profit, and contains a variety of features that are advantageous in dealing with the many competing considerations in a liquidating trust. To the extent that the persons winding up the debtor or other liquidating entity may have claims to pursue or defend, a DST is a separate legal entity. The DST Act permits a trustee to take direction from other parties, whether beneficiaries, advisors, a grantor or other interested or independent parties. Thus a management or oversight committee may be appointed to make certain determinations, to monitor the trustee's activities. The DST Act also empowers a trustee to delegate some or nearly all of its powers without rendering the delegee liable as a trustee. Of critical importance are the provisions of the DST Act permitting drafters of a trust governing instrument to restrict, modify or eliminate fiduciary duties of trustees and other persons managing a DST, subject to the implied contractual

covenant of good faith and fair dealing.

The annual maintenance costs for a DST are fairly nominal - the trust pays no annual maintenance fee to the Delaware Secretary of State. In addition to the fees payable to the liquidating agent, or liquidating trustee, if the liquidating trustee is not an individual Delaware resident, or a Delaware banking institution or trust company or federally chartered bank or trust company with its principal place of business in Delaware, the trust will need to engage a trustee meeting that description. Fortunately, there are individuals and institutions in Delaware that make a business of providing Delaware statutory trustee services for a fairly nominal fee (a few thousand dollars a year) who will undertake the limited role of qualifying the trust as a DST. Of course, many local banking institutions will also provide the more substantive services, for a higher fee.

Additional factors to consider include tax and securities implications. As noted above, most liquidation trusts are structured as grantor trusts for tax purposes, and the IRS has established standards pursuant to Treas. Reg. 301.7701-4(d) applicable to liquidating trusts that, if followed, should ensure that they are not subject to entity-level income taxes. If the trust term will be longer than a few years, it may be prudent to seek an IRS determination letter that the trust will qualify for grantor trust tax treatment. In addition, where a public company with over $10,000,000 in assets at least one registered class of securities held by at least 500 stockholders, consideration must be given to whether the interests in the liquidating trust will be "equity securities" such that the trust must register the interest with the Securities and

Exchange Commission. For these and other reasons, it is important to secure experienced professionals to assist with the formation of a liquidation trust.

Bayard's entity law group has experience working with the full array of Delaware business organizations, including statutory trusts, corporations, general partnerships, limited partnerships, limited liability partnerships and limited liability companies. Each of these entity types presents different considerations as to establishment, operation, management, liability, scope of authority and dissolution. While Delaware corporations are highly regarded due to Delaware's progressive and regularly updated corporate statutes, the substantial body of interpretive case law, which promotes predictability, specialized and well-respected Delaware Court of Chancery and responsive and technologically advanced Division of Corporations, Delaware alternative entities are known for their flexibility and share in a growing body of case law, and the benefits of access to the Court of Chancery and Division of Corporations. Bayard also has experienced litigators capable of handling a variety of entity law litigation matters, including seeking the appointment of receivers for dissolved companies and seeking approval of a corporate plan of liquidation under the so called "safe harbor" liquidation procedures. For questions regarding Delaware entity law, please contact Marla Norton at (302) 429-4214 or MNorton@bayardlaw.com.

For your convenience we are providing an excerpt of a chart we have prepared which provides an overview the different features of each entity type, highlighting the default rules relating to liquidation and winding up of each. The full table can be viewed on Bayard's web site at www.bayardlaw.com.

First published in Lawyer Monthly, March 2014. Link to article.